How the Big Tech monster is saving global indices

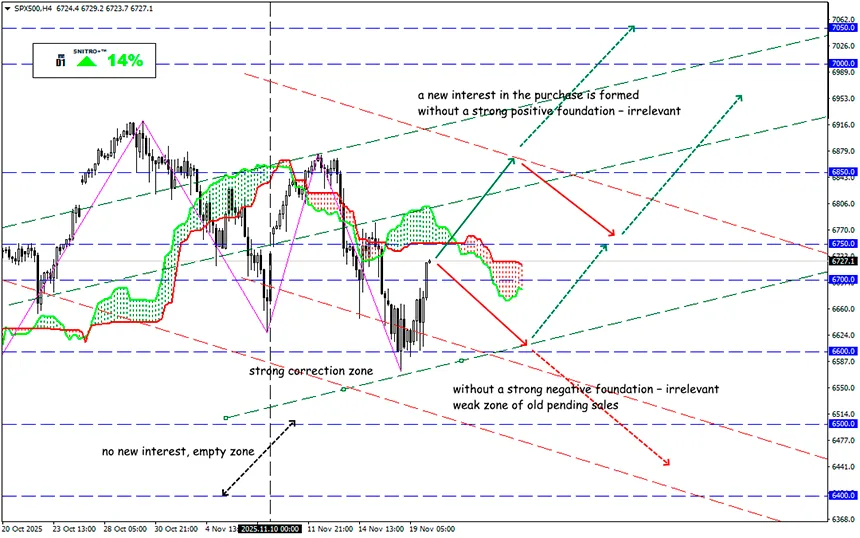

SP500

Key zone: 6,650 - 6,750

Buy: 6,800 (on a confident breakout of the 6,750 level); target 6,900-6,950; StopLoss 6,720

Sell: 6,650(on strong negative fundamentals); target 6,500; StopLoss 6,720

Nvidia didn’t even need a buyback to secure an ultra-bullish market reaction. The main speculative move will come today after the U.S. market opens. At the same time, there will be no additional real money on the market (especially on the crypto side), because NVDA’s numbers are largely the result of multiplying the same capital on paper.

Recall: Nvidia “gives” money (effectively sponsors) OpenAI and other companies (such as the Anthropic deal) so that they buy its proprietary high-performance chips. In this way Nvidia boosts future profits from sales of its own chips that were originally bought with its own money. The company uses such methods on a permanent basis and quite efficiently.

Here are the key metrics:

- Revenue came in at ≈ $57.0 bn, well above expectations (~$54.9 bn), reflecting 62% y/y growth.

- Earnings per share (EPS) – $1.30 versus expectations of $1.25.

- The Data Center/AI segment delivered revenue of about $51.2 bn, above forecasts.

- Management issued an upbeat outlook for Q4: more than $65 bn in revenue, above expectations of $61–62 bn.

- NVDA shares are up about 6% in post-market trading.

Where is the positive side of this report?

- The beats on revenue and EPS confirm that demand for Nvidia’s AI infrastructure remains very strong.

- Strong growth in the Data Center segment shows that optimism is backed by real corporate capex – this is the key sign that the trend is structurally supported.

- Guidance for the next quarter is above what the market expected – management sees a continued growth trajectory rather than a one-off spike.

- Against the backdrop of rising concerns about an “AI bubble”, this report gives markets a short-term dose of reassurance: demand trackers, contracts and new architectures (for example, next-gen chips) are all working effectively.

What is the risk for Nvidia that cannot be ignored?

- Despite 62% growth, the share price already discounts very high “future profits”. Even a strong print may not be enough if there is no confidence that the positive trend will continue.

- Management (and the media) highlighted potential headwinds: energy constraints, export restrictions (especially to China) and the scale of infrastructure spending.

- If the next quarters show slower growth or decelerating momentum, Nvidia’s valuation multiples (P/E, P/S) may become a problem – the probability of a correction is high.

- Rising competition (Advanced Micro Devices, Inc., Intel Corporation), saturation of the AI-infrastructure market, and growing costs (power, cooling, talent) will all weigh on the growth pace.

What does this report mean for a trader?

- Positioning: If you trade NVDA or the semiconductor sector, this report supports the base case that “AI infrastructure is still in expansion mode”. But you should not buy without tight protection – high volatility is likely.

- Hedging: After a strong report, a technical pullback is almost inevitable; the key risk is that elevated expectations for Nvidia will keep being priced in over future quarters. That makes StopLosses or options mandatory.

- Time horizon: If your strategy is short-term (H1–W1), you can trade off the market reaction: upside is possible, but so is a follow-up correction on “disappointing details”. If it is medium-term, focus on sector-wide trends rather than a single quarter’s numbers.

Nvidia’s report is genuinely strong: revenue and earnings are above expectations, and guidance is confident. As Nvidia is treated as a “barometer” of AI infrastructure, its positive results lower system-wide risk for other names in the space; weak signals would do the opposite. Traders should closely watch how competitors and adjacent companies react.

So we act wisely and avoid unnecessary risks.

Profits to y’all!