The Bank of England is not ready to take risks

Is a BOE rate hike possible?

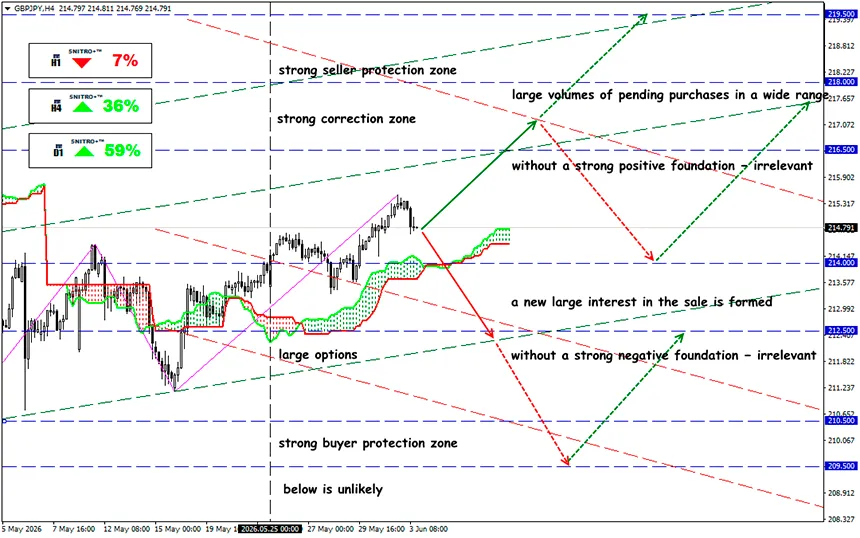

GBP/JPY

Key zone: 214.00 - 215.50

Buy: 216.00 (on a strong positive foundation); target 218.50-219.00; StopLoss 215.40

Sell: 213.50 (following a decisive break above the 214 level) ; target 211.50-210.00; StopLoss 214.20

The threat of a Bank of England interest rate hike at the next meeting and the unclear outlook for British monetary policy continue to unsettle the market. The next meeting on June 18 will be an event with asymmetric risk for the GBP segment.

Domestic policy is working against a hardline move. Keir Starmer’s government and Chancellor Rachel Reeves are betting on “stability,” investment, and fiscal discipline. However, the growing tax burden on business and higher labor costs are increasing pressure on employment in retail, HoReCa, and small business. In other words, monetary tightening may now overlap with a destructive fiscal impulse.

Let us recall:

For the currency market, what matters is not the rate itself, but the difference between the actual decision and what is already priced in. The current base-case scenario is that the BOE Bank Rate remains at 3.75% with a hawkish accompanying statement. The GBP reaction will depend on the degree of deviation from this scenario. But the risk is rising: the inflation background has worsened, and some MPC officials openly allow for the need to tighten policy.

Factors the monetary regulator uses to make its decision:

- The main argument “in favor” of a hike is inflation. CPI in April fell to 2.8% after 3.3% in March, but the structure of the data remains unpleasant: CPIH — 3.0%, core CPIH — 2.8%, transport — 4.5%, communications — 4.5%, restaurants and hotels — 4.4%. Services slowed to 3.4%, but this is still above the level compatible with the 2% target. The energy shock has already pushed fuel prices higher and may strengthen second-round effects in wages and prices.

- The labor market is sending a mixed signal. Unemployment remains around 4.9–5.0%, but vacancies are declining: 705,000 in February–April versus 759,000 a year earlier. Nominal wage growth slowed to about 3.6%, while real wages are nearly stagnating. This is an argument against an aggressive hike: domestic demand is cooling, and labor market overheating is no longer obvious.

- Economic activity is weak. GDP remained fragile in March, while the May PMI showed a sharp deterioration: the composite index was around 48.5, with services below 50. This is especially important because services account for around 80% of the British economy. GDP growth is expected at only 0.9% in 2026, with unemployment rising to 5.5%. Such a backdrop makes a rate hike risky for real estate and consumption.

The conflict in the Middle East threatens supplies of oil, gas, diesel, and jet fuel. Rising oil supports inflation expectations and gilt yields but weighs on FTSE sectors dependent on domestic demand. If oil holds above $90, it will be difficult for the regulator to justify keeping the rate unchanged for a long time without raising it.

And what is the result?

The probability of a rate hike at the next meeting can be estimated at 25–35%. A hike to 4.00% is possible only if the MPC sees the energy shock as the beginning of a new inflationary wave rather than a temporary factor. A full-fledged tightening cycle remains unlikely for now.

Of course, GBP is receiving support from expectations of tighter monetary policy, which would be a strong bullish signal; however, weak PMI and recession risk limit the pound’s upside potential.

But without confirmation of persistent services inflation, the move may quickly turn into profit-taking. If a pause is decided, but the number of supporters of a hike rises from 1 to 2–3 people, the market may react almost the same way as to an actual rate hike.

For GBP/JPY, this is the currency pair most sensitive to any surprise from the BOE, and the effect will be even stronger. The Bank of Japan maintains an extremely soft policy, while Japanese rates remain near zero. Even moderate BoE tightening sharply increases the carry attractiveness of the pound.

So we act wisely and avoid unnecessary risks.

Profits to y’all!