Europe seeks optimal balance

The ECB and Bank of England are ready to adjust rates

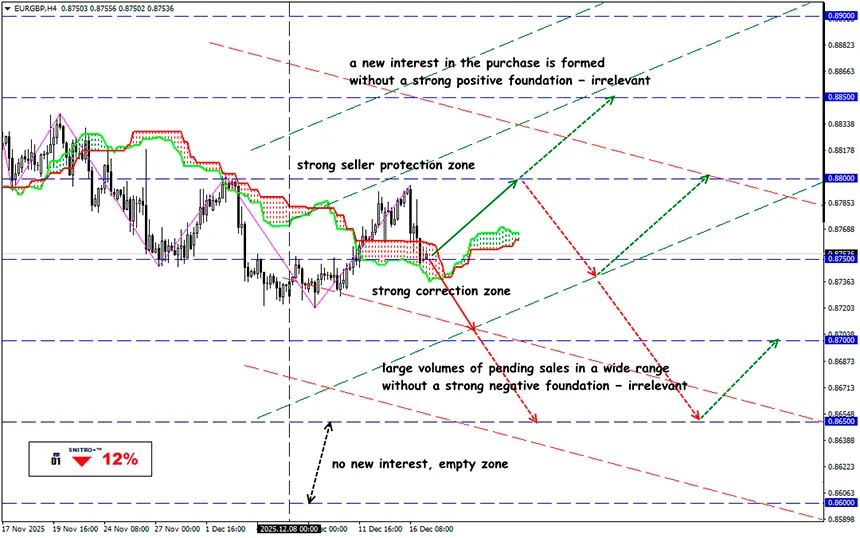

EUR/GBP

Key zone: 0.8750 - 0.8800

Buy: 0.8800 (on strong positive fundamentals) ; target 0.8900-0.8950; StopLoss 0.8760

Sell: 0.8740 (after retesting the 0.8780 level) ; target 0.8600; StopLoss 0.8780

Major European monetary regulators are deciding on interest rates, which will determine the trend for the EUR and GBP for at least the first quarter of 2026. That is, of course, unless some force majeure adds negativity to the fundamental background for the dollar.

The latest statistics on the euro and the pound support the idea of a rate adjustment, but the market has already factored almost everything into the current price. Participants are not risking opening large positions, but are actively removing StopLoss on both sides of the market.

As a reminder, in addition to geopolitics, the dollar is under pressure due to expectations of two more Fed interest rate cuts. And no matter how European assets try to maneuver between their problems, they will also have to respond to this threat.

Data from S&P Global showed that private sector activity in the eurozone grew less than expected in December this year, as Germany's industrial sector unexpectedly deteriorated. According to the data, the composite eurozone purchasing managers' index fell to 51.9 from 52.8 in November, remaining above the 50 threshold that separates growth from contraction.

The decline in the eurozone PMI indicates a slowdown in growth in the region, although it remains positive.

Despite these data, the ECB is unlikely to decide to change the rate: the weakening of the PMI index may be due to several factors, including US tariffs, core inflation, and geopolitical uncertainty. In other words, all the negative factors are interpreted as short-term.

- ECB

Europe, represented by Lagarde, is clearly moving towards tightening expectations (inflation forecasts and comments from officials), but there is not enough of a sharp deterioration in retail demand and the labor market or a fall in inflation below forecasts to justify a rate correction.

Base scenario: we maintain the rate at 2.00%, with an accompanying statement without sharply optimistic comments. The situation is supported by the fact that inflation in the eurozone is close to target, and growth is weak but not dangerous.

Key risk for the EUR: not a pause in the rate correction, but the tone of the press conference + the trajectory of forecasts (inflation path / wage dynamics / restrictive enough). But! If the market has overestimated the pace of easing, we will see a strong short squeeze on EUR/USD.

BOE:

The deterioration in labor market indicators + pressure on wages require a rate cut, but at the same time, control over inflation must not be lost. In addition to the rate level, we are assessing the distribution of votes, looking for phrases about the labor market and services in the accompanying statement, and listening carefully to Bailey's speech.

The market estimates the probability of a 25 bp cut (from 4.00% to 3.75%) at 85%, with a close vote (conditionally 5-4) being discussed.

The key risk for GBP is that if inflation/services prove problematic, the BoE may hold rates or give a less positive signal than market expectations. The situation could play out as a strong short squeeze for GBP/USD.

EUR/GBP will be a stronger and more stable asset tomorrow, as there will be no market "noise" from the dollar, but there will be maximum divergence between the ECB and the BOE, i.e.:

- Neutral ECB stance + soft Bank of England stance – upward trend for EUR/GBP

- Soft ECB stance + hawkish Bank of England stance – reversal of the EUR/GBP rate

Given that the ECB will keep its rate unchanged and the BOE will cut its rate, the most likely direction for EUR/GBP is up (the euro looks stronger than the pound).

Tactics: wait for both decisions and trade the second wave 15-30 minutes after the BOE.

So we act wisely and avoid unnecessary risks.

Profits to y’all!