Stablecoins: a shield against hyperinflation

Can digital dollars replace paper cash?

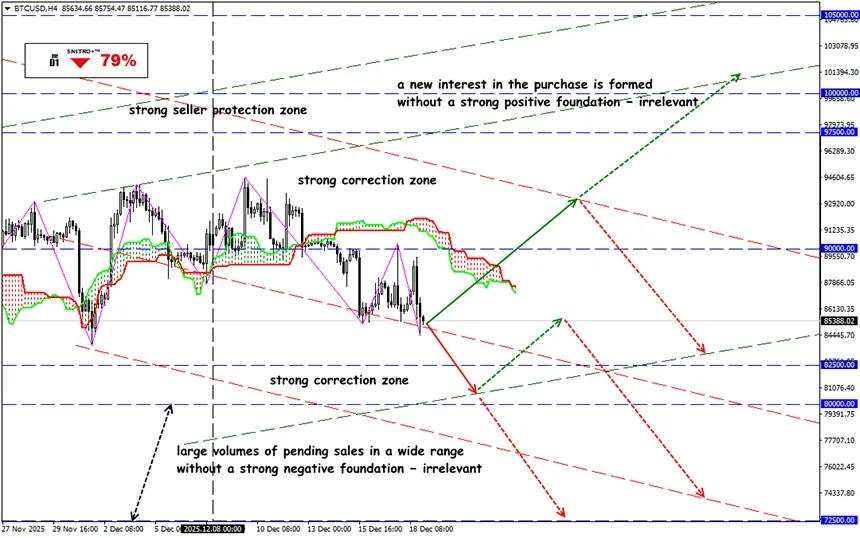

BTC/USD

Key zone: 83,500 - 87,000

Buy: 87,500 (after retesting the 90,000 level) ; target 90,000-93,500; StopLoss 86,500

Sell: 82,500 (on strong negative fundamentals) ; target 80,000-78,500; StopLoss 83,500

In countries with chronic inflation, capital controls, and limited access to dollar liquidity, stablecoins are becoming a full-fledged element of the financial system. They perform the functions of money where national currencies have lost trust and the banking system cannot handle basic tasks.

And this is not about speculators. In hyperinflationary countries, crypto tokens are used as a store of value and a unit of account, compensating for the unavailability of physical dollars and the inefficiency of local payment systems.

Reminder:

In unstable conditions, the priority is not currency yield, but nominal stability and liquidity. Volatile cryptocurrencies are poorly suited for everyday payments and short-term savings (just look at what’s happening with Bitcoin). Stablecoins, on the other hand, let users lock value in USD without banks and without currency restrictions.

A physical dollar formally serves the same function, but in practice its use is complicated by:

- capital controls;

- withdrawal limits;

- cash shortages;

- multiple exchange rates;

- a gap between the official and market rate;

- technical and political sanctions, etc.

When problems escalate, cash-dollar transactions quickly move into the “shadow” sector, raising costs and risks. USDT or USDC do not require a bank account, enable direct transfers, and do not depend on local infrastructure.

By 2025, the stablecoin market capitalization approached $300 billion — about 30% of all crypto transactions are in stablecoins, and a significant share of that volume is generated in countries with currency instability.

Countries where stablecoins have become part of the economy:

Venezuela

Years of hyperinflation destroyed trust in the national currency (VEF), and the country now ranks in the top 20 for crypto adoption. Most turnover goes through P2P platforms rather than centralized exchanges. Businesses increasingly accept USDT as an alternative to the national currency due to limited access to physical dollars. In effect, a parallel payments infrastructure is forming, independent of the domestic financial system.

Argentina

Crypto demand formed amid capital controls and chronic peso devaluation. In Argentina, about 18% of the population uses cryptocurrencies — the highest figure in the region. Stablecoins are integrated into payment services, used in e-commerce, and embedded in savings products. This is supported by a large unbanked population and high fees for international transfers.

Nigeria

As an alternative to the state token eNaira, which never became a mass payment instrument, a regulated private stablecoin cNGN was launched. The project is implemented under the supervision of financial regulators and positioned as an alternative blockchain-based payment layer.

Of course, growing stablecoin popularity does not eliminate macroeconomic imbalances. Stablecoins:

- do not replace structural reforms;

- do not stop inflation;

- do not stabilize public finances.

However, at the household and small-business level, they are a workable adaptation mechanism that reduces losses from devaluation and bypasses inefficient payment systems.

In parallel, a new infrastructure layer is forming:

- payment cards linked to stablecoins;

- partnerships with global payment networks;

- instant cross-border transfer services with low fees.

This gradually blurs the boundary between traditional finance and blockchain.

In hyperinflationary countries, stablecoins serve a technical function — access to stable money, not investment. They remain a risky element of the financial system and do not solve macroeconomic problems, but they allow users to retain access to capital in an unstable economic environment.

So we act wisely and avoid unnecessary risks.

Profits to y’all!