Europe prepares a surprise for Trump

The stock market is looking for protection from U.S. aggression

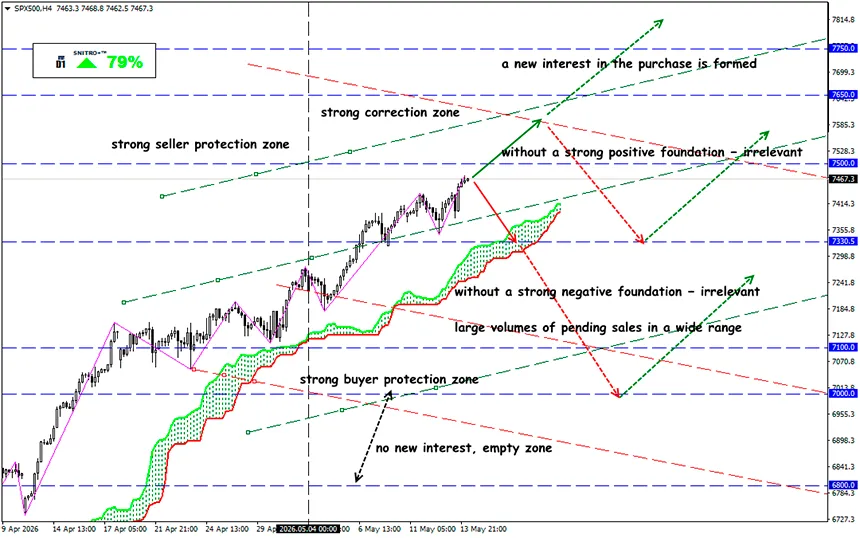

SP500

Key zone: 7,400 - 7,500

Buy: 7,550 (on a decisive break of 7,500); target 7,650-7,700; StopLoss 7,500

Sell: 7,350 (on strong negative fundamentals); target 7,150; StopLoss 7,420

The European securities depository Euroclear is considering the use of Chinese bonds as collateral for financial transactions. If implemented, the initiative would mark an important step toward integrating China’s debt market into the global financial infrastructure and increase the attractiveness of Chinese assets for international investors.

Reminder:

European equities are significantly cheaper in terms of valuation multiples and tend to react more strongly to a recovery in global trade. During periods of global stress, capital often exits European assets and moves into U.S. securities. The exception is the British market (FTSE 100 index), which is less dependent on China and more exposed to oil and commodities.

The discussion now focuses on Chinese government bonds and high-quality corporate debt that could be used by market participants as collateral for transactions, liquidity management, and broader applications in international settlements and repo operations across global capital markets.

Such a move could strengthen the role of Chinese debt instruments, although implementation will depend on risk assessment. That process currently carries a strong political dimension.

Why does this matter for markets?

Recognition of these assets by one of Europe’s key clearing and settlement infrastructures could elevate the status of Chinese bonds among global investors and financial institutions.

The ability to use bonds as collateral makes them a more functional instrument rather than simply an investment vehicle, which typically boosts interest from banks, funds, asset managers, and private investors.

Against the backdrop of geopolitical fragmentation and a reassessment of currency risks, market participants continue to search for alternative high-quality assets outside the traditional pool of dollar- and euro-denominated securities.

This is a major argument in favor of internationalizing China’s financial market and gradually strengthening yuan-denominated assets. However, transparency concerns, credit risks, cross-border regulations, and the willingness of international participants to actively use Chinese securities as business guarantees remain key limitations.

If Euroclear launches such a practice, markets could receive a signal of the gradual increase in the “acceptability” of Chinese bonds — not only as investment assets but also as fully functional settlement instruments.

For global equity markets, Trump’s visit to China is not merely a diplomatic event. It represents a potential reassessment point for:

- global growth;

- world trade;

- supply chains;

- the technology sector;

- the risk of a new Cold Economic War.

Stock markets will react not to the fact of the meeting itself, but to the answer to one question: are the U.S. and China moving toward managed competition, or is the world entering a phase of accelerated economic fragmentation? That will determine the direction of U.S., European, and Asian equities for months ahead.

What does this mean in practice?

The U.S. stock market is less dependent on China than Europe or Asia. However, the United States remains the center of the global tech sector, the core of AI infrastructure, and the issuer of the world’s reserve currency.

For the S&P 500, a positive summit outcome (trade war postponed, supply chains preserved, etc.) would be a major bullish catalyst. This is especially important for giants such as Apple, Nvidia, AMD, Qualcomm, Tesla, Microsoft, Amazon, Meta, Caterpillar, Boeing, Nike, and Starbucks.

Right now, institutional capital fears not a U.S. recession, but tariff escalation, pressure on Big Tech, supply chain disruptions, and a geopolitical shock to commodity markets. If talks fail, markets will begin pricing in the risks of higher tariffs, slower global trade, and a new technological “war.”

So we act wisely and avoid unnecessary risks.

Profits to y’all!