Fair of mistrust or difficulty of currency transfer

The European creditors and the IMF reached the agreement about a common position concerning Greece at last

The market doesn't trust any more: in a raising of FRS rates, in soft Brexit, weak dollar, cheap oil, the Chinese statistics, Trump`s immigrant policy and tax promises. Now everyone comments the currency rates, it disturbs real estimates and increases the risk of any transactions against the background of weak volatility.

The process of adoption of the British bill under article 50, where after the ratification of the lower house discussion was transferred to the Senate, holds the attention of the European investors. The amendment granting the right to residents of the EU to live in Great Britain is already rejected. It is doubtful the following amendment will be adopted − about putting the draft agreement with the EU on the referendum, but now any obstacles concerning Brexit will promote the growth of pound. Though the currency began to be nervous after a decrease in BoE forecasts for inflation growth − on data on the labor market and on retail sales there can be active speculation.

The European creditors and the IMF reached the agreement about a common position concerning Greece at last, however still it is unknown whether Greece will accept the new offer, it can be seen later. Draghi's declamation during the performance in European Parliament and radical statements of Marine Le Pen about a possible exit of France from a zone of the EU unexpectedly came into the view of the investors, if is more specific – about the procedure and cost of an exit from the eurozone. Anyway, the head of the ECB tried to emphasize very much that there is no way back for those who entered the eurozone. At least, because of it is very expensive. Speculation on this subject increases interest in the release and comments under the protocol of the European Central Bank from a meeting on January 19.

The staff of the government of Scotland was ordered to begin preparation for the second referendum on independence within 2 weeks, but the European Commission representative already declared that independent Scotland will be required get in a line for membership in the EU in a general order.

Analysts expected the beginning of Brexit can be postponed until the end of September when in Germany take place elections of the new chancellor as there is no sense to agree with the operating governments when if the new power, perhaps, isn't ready to adhere to them. Thus, May can have over a year to reach the agreement with the European Union till March 2019.

If Brexit passes quickly/successfully, it can affect other countries, such as Finland and the Netherlands which are more and more hostile in relation to the EU. Great Britain should resolve the mass of issues on the concession on free movement of people or legislative restrictions during the long period, and the EU is interested in a transition period and preserving the relations with the Kingdom – as protection of the block.

Now all markets were concentrated on Trump, but the events which are taking place on another side of the world can be much more significant. China started the program of the budget incentives and finances it by the sale of land by local governments and a boom in the real estate market. The Chinese business cycle already went to growth and quickly accelerates since the beginning of the year. Germany showed the maximum export volume to the east, the USA and other countries of the G7 joined this impulse, that is the main reason for the current optimism is the Chinese political solutions of last year at all but not hopes for changes in policy of the USA.

The Central Bank of China which continues devaluation of yuan against the dollar and the block of strong data last week, strengthening of control of capital outflow, mitigation of Trump`s rhetoric shifted the beginning of the Chinese stock market collapse for the later period, but you shouldn`t relax. We monitor data on inflation growth in the Tuesday`s morning. Though Trump continues to speculate in the style – promised «something phenomenal concerning taxes in the next 2-3 weeks» − the large equity expects impressive tax remissions which will potentially support the economy. There is a hope that the president, after all, will switch from empty protectionist attacks to internal economic problems.

At first sight the report on accomplishment of the US budget looks not bad: in January the Treasury gained income in the amount of $344 billion, and its expenses constituted only $293 billion, therefore, monthly surplus was equal much more the being expected $40 billion (much more last year's deficit in $28 billion). But this surplus is received generally for the account of the law requiring from Tax administration to detain sending of checks with compensation amounts of taxes to the households which declared the rights to them. The real budget deficit in the current financial year (for January 31) made $157 billion, and it will increase within half a year, at least.

FRS speakers will be able to influence the markets only if their expectations is confirmed with Yellen`s rhetoric in the semi-annual report in the Congress of the USA (on Tuesday in the Senate, on Wednesday in − to the House of Representatives). Yellen's answers to questions of congressmen will be most important, in particular about a possibility of acceleration of rates increase in the case of implementation of fiscal incentives of Trump. If lady Janet, even tactful, will hint on a gradual increase in rates, then the market will ignore other ideas.

Oil grew on optimism on the performance of the OPEC agreement (and out of it) on reducing production. Never before the world oil cartel fulfilled the obligations so quickly – according to the report of IEA the OPEC countries in January reduced production by 1 million barrels a day, i.e. for 90% of the reached agreement. The monthly report of OPEC on Monday will become the major event for oil.

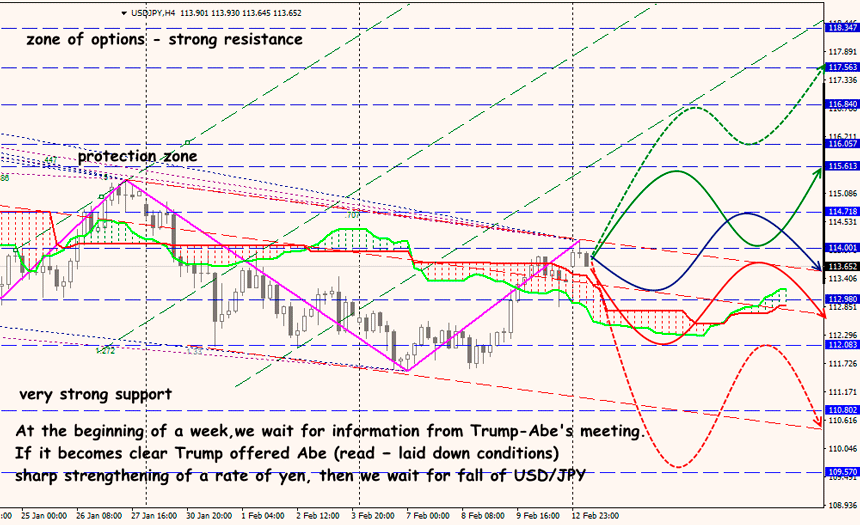

The question concerning currency devaluation against dollar was raised during the joint press conference of Trump and the prime minister of Japan Abe. Not for nothing Abe took the Minister of Finance Aso on this golf game in the private residence. Besides, Japan is ready to offer Trump investments into the infrastructure of the USA for the sake of smoothing of the conflict. Anyway, currency wars keep on the priority list of the new administration of the White House, that`s confirmed by Trump's answers. A detailed discussion of currency claims of the USA to Japan and other countries will happen at the summit of the G20 Ministries of Finance and heads of the Central Bank on March 17-18 and it is necessary to expect fall of dollar exchange rate in the run-up to this summit.

There no expected important events in the plan for the next week, therefore, it is necessary to be guided by the general provision of things: ECB doesn't change policy, and FRS aggressively tries to prove it will begin toughening. The main claims of the new American president to a manipulation currency rates equally concern Japan, China and the Eurozone.

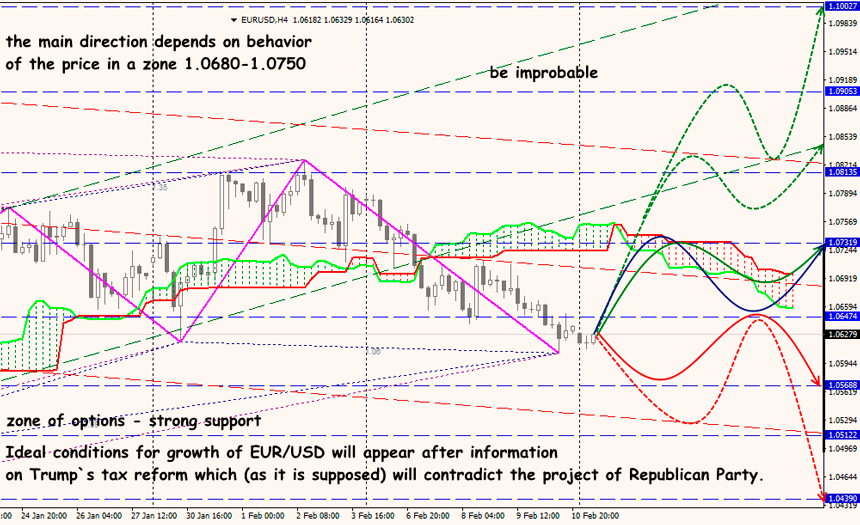

Technical Analysis EUR/USD

Technical Analysis USD/JPY