Auction of miracles is closed: who received the bonus?

OPEC + updated the terms of the deal, Fed and ECB maintained rates, Johnson won the election and promised to close the Brexit topic in two weeks. The final flourish: US-China trade truce. All events have passed, but not all goals have been achieved.

Philosophers believe that «A wonder lasts but nine days», but the events of the past week will be enough for the financial markets for a long time. So…

Pound & Brexit

The Tories received the necessary majority in the lower house of the British Parliament, so the opinion of the Eurosceptics on the adoption of government bills can not affect. Corbin promised the electorate his resignation, and SNP considers his party’s result to be a real victory: 48 (45.0%) out of 59 possible mandates. Nicola Sturgeon is confident that the British Prime Minister has a mandate for Brexit only in England, but does not have the right to «disconnect» Scotland from the European Union. The topic of a new referendum on independence from Britain is actively lobbying and runs the risk of becoming a serious problem for Johnson. Next week, SNP will file an official application, but the chances of approving this process are meagre.

Parliament's ratification of the current Brexit option is not in doubt, although the debate will officially resume after the Queen’s speech on Thursday. By January 31, London and Brussels should begin the «transition period» with an approximate period until the end of 2020, but to solve all the problems for the year is unrealistic. Recall that the EU trade agreement with Canada has been preparing for almost 7 years.

Negotiating a trade deal will still be difficult. The current version of the agreement takes into account all the permissible concessions to Britain, thanks to which London could bargain with the EU, there will be no correction of conditions. Ratification will provide everything the European Union needs, London’s access to the WTO (if the WTO, of course, survives the fight against Trump) will hit the British economy, but there is still a chance that the trade agreement will be as loyal as possible. Johnson logically fears that if the deal with the EU is too soft, Trump may refuse a profitable bilateral agreement, but there is no other way out.

The focus of attention is aimed at the BOE meeting, we are waiting for an assessment of the consequences of the ratification of the Brexit agreement, but Carney no longer makes sense to declare a policy correction. Johnson plans to replace the head of the Central Bank in the coming weeks, the most likely candidate is Minouche Shafik, whose rhetoric will have a strong impact on the dynamics of the pound.

USA & China

December - too inconvenient time for new sanctions, but the stock market. The USA at maximum an excellent Christmas present for the country from the main storyteller. Finally, Trump recognized the danger of trade wars in the election year and this fact is an absolute positive for the global economy. Asian excerpts brought results - today there will be no increase in duties. But there are nuances ...

- very old arrangements without details were voiced;

- there is no general («nominal», according to Trump) document when it will be - unclear;

- The USA lifts only a small portion of the sanctions;

- $120 billion import duties introduced in September are reduced from 15% to 7.5 (no confirmation);

- Lighthizer said that China agrees to increase the import of US goods and services by (at least!) $200 billion over the next two years, but there will be no guarantees in the official document;

- The second phase of negotiations is planned after the US presidential election (interest in tweet-Trump has already decreased);

- China is committed to protecting intellectual property, transferring technology, controlling the financial sector and the renminbi.

And now, obverse case:

- 25% duties on China's imports of $250 billion per year will remain, and maybe discussed not earlier than next fall;

- «other tariffs», as Trump put it, also «mostly preserved»;

- China reiterated that it «hopes for the United States to fulfil all the agreements», obviously, on the Huawei problem - the new agreement provides for the observance of the legal rights of companies of both parties in both territories;

- The issue of quotas for the import of duty-free goods has not been resolved, that is, even when a new transaction is completed, US customs may delay the import of any goods for observing intellectual property rights;

- The Chinese side «asked» not to make the text of the document public, so as not to irritate public opinion, and most likely there will not be a ceremony of signing the document by Trump and Xi.

Conclusion: until January, the situation (as in a fairy tale!) may well change several more times and the trade war will not be cancelled next year.

FRS

The results of the last meeting will contribute to an increase in risk appetite against the backdrop of a falling dollar, even though the point forecasts of Fed members do not contain intentions to further reduce rates. The strong November NFP shifted concerns toward a possible tightening of the Fed's policy, and Powell’s press conference resembled a children's New Year’s show with presents. The most urgent task is to provide markets with dollar liquidity by the end of the year. Markets are ready to put up with the lack of prospects for rate adjustments, while the Fed (in fact!) implements the QE4 program with the purchase of US T-bills in portions of $60 billion a month.

The promise to reduce repurchase transactions at the beginning of 2020 implies a correction for the growth of the dollar in the second half of January, unless, of course, other factors appear to depreciate.

ECB

The policy of the Eurobank is unchanged, the September stimulus package will not be reviewed, the rhetoric of Lagarde confirms the continuity with Draghi. But there are some differences:

- some first signs of a slowdown in production and a slight increase in core inflation were recorded;

- Risks for the prospects for the Eurozone economy are still aimed at lowering;

- further easing of the policy is extremely unlikely, trade negotiations between the US and China reinforce the general positive;

- when revising economic forecasts for an increase in the ECB, it may change the size of excess reserves of banks exempted from the negative rate, which will be equivalent to an increase in the general rate;

- a strategic review of the ECB policy and discussion of non-traditional instruments of monetary regulation are expected in January.

The House of Representatives must vote on a government funding bill to avoid a shutdown after December 20. $1.375 billion of financing the wall on the border with Mexico remain a condition between the party deal. However, Trump will retain the ability to transfer funds from other budget items, which is now the subject of litigation. U.S. lower house voting on the impeachment of Trump is scheduled for Wednesday, but markets will be short-term. The Judicial Committee of the House of Representatives formed a new decision, despite the objections and amendments of the Republican Party, but everyone understands that the Senate will not support impeachment. The meaning of this action is not as a result but in a constant destabilizing process.

This week we pay attention to statistics:

- USA - PMI industry and services, consumer spending inflation, US GDP for the 3rd quarter, Philadelphia Fed manufacturing index;

- Eurozone - Germany IFO Index; PMI industry and services (Dec); consumer price inflation (Nov);

- UK - PMI industry and services, inflation and labour market reports, retail sales and BOE.

Morning statistics of China turned out to be neutral positive, the impact on Asian assets is minimal.

Important speeches by Fed officials are not planned before the end of the year; Lagarde will deliver a speech at a reception in honour of Kere's resignation, but no surprises are expected. On Wednesday, an intermediate meeting of the ECB will take place, we are waiting for the traditional portion of insider trading.

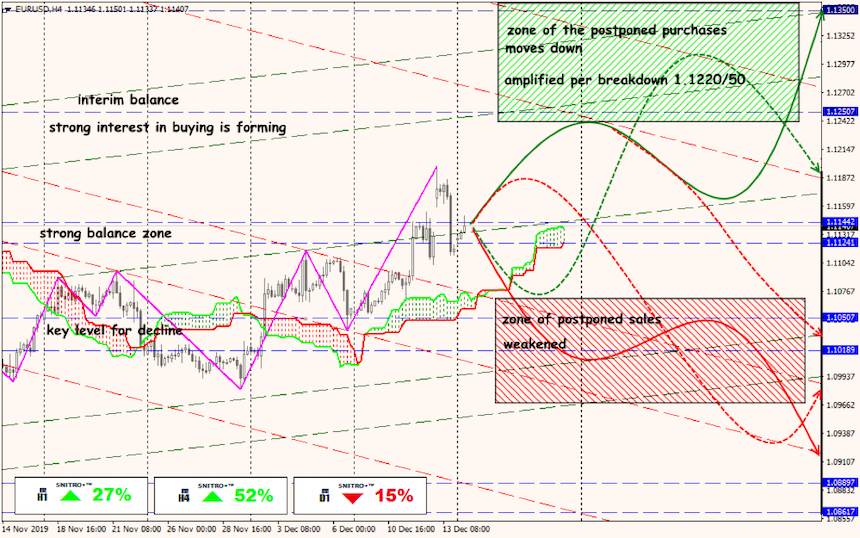

Technical Analysis EUR/USD

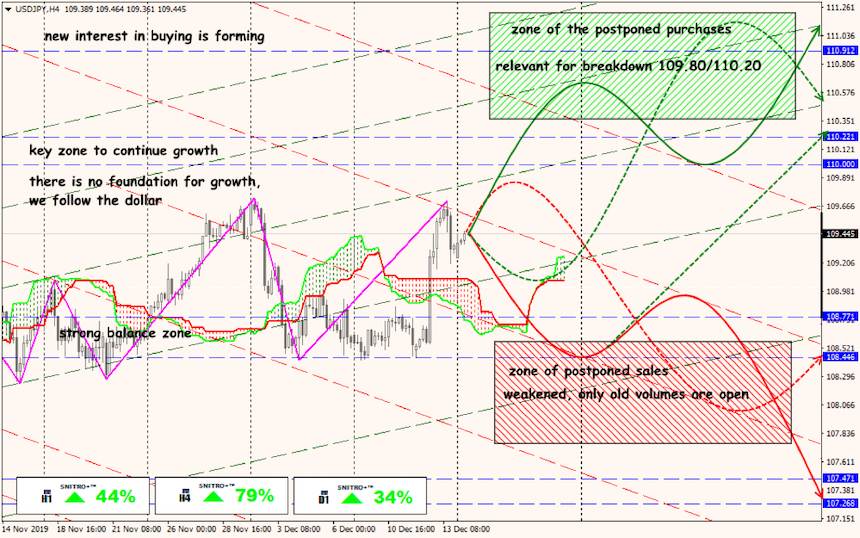

Technical Analysis USD/JPY

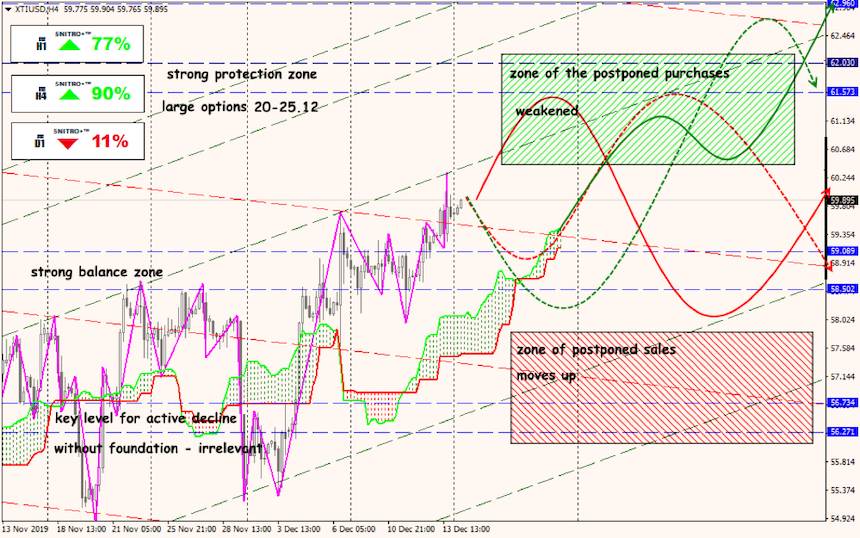

Technical Analysis XTI/USD