Europe prepares a surprise for Trump

The stock market is looking for protection from U.S. aggression

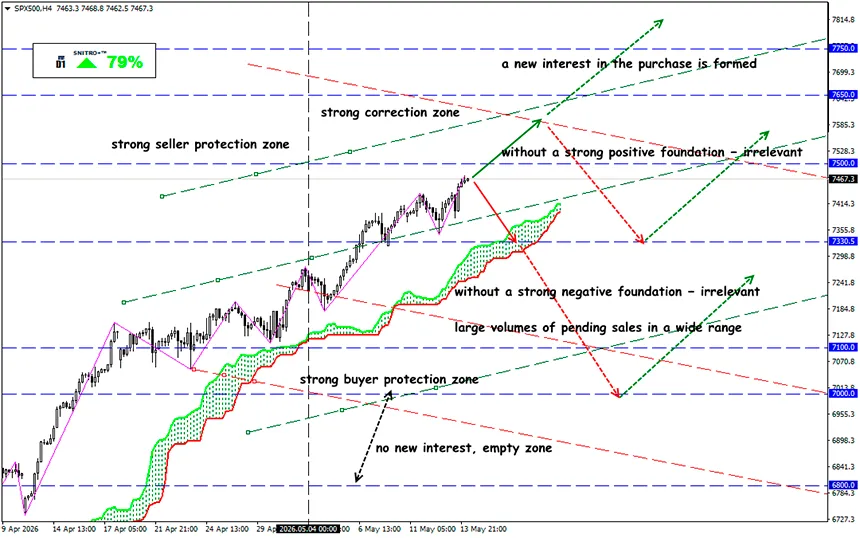

SP500

Key zone: 7,400 - 7,500

Buy: 7,550 (on a decisive break of 7,500); target 7,650-7,700; StopLoss 7,500

Sell: 7,350 (on strong negative fundamentals); target 7,150; StopLoss 7,420

Europe may be preparing one of the most important financial shifts of recent years. European securities depository Euroclear is discussing the possibility of accepting Chinese bonds as collateral for financial transactions. If implemented, this would become a significant step toward integrating China’s debt market into the global financial system and could strengthen the position of Chinese assets among international investors.

Reminder:

European equities remain significantly cheaper than U.S. stocks in terms of valuation multiples and usually react more aggressively to any recovery in global trade. During periods of stress, capital traditionally flows out of Europe into U.S. assets. The main exception is the British FTSE 100, which is less dependent on China and more closely tied to commodity and energy sectors.

The current discussion concerns Chinese government bonds and high-grade corporate debt that could potentially be used as collateral in repo transactions, liquidity management operations, and international settlements across global capital markets.

If such a mechanism is approved, Chinese debt instruments would gain a new role — not merely as investment assets, but as part of the core infrastructure of global finance.

At the same time, implementation depends heavily on political and risk-related considerations. Questions around transparency, regulation, credit risks, and the willingness of Western institutions to actively use Chinese assets remain unresolved.

Why markets care about this

Recognition by one of Europe’s largest clearing infrastructures would significantly improve the status of Chinese debt instruments in the eyes of banks, funds, and institutional investors.

The ability to use bonds as collateral transforms them from passive investments into functional financial instruments, increasing their attractiveness for trading, liquidity operations, and portfolio management.

Against the backdrop of geopolitical fragmentation and growing concerns over dollar dependence, investors are increasingly searching for alternative reserve-quality assets outside the traditional U.S. dollar and euro system.

This would support the long-term internationalization of yuan-denominated assets and gradually expand China’s influence within the global financial architecture.

If Euroclear proceeds with this initiative, markets may interpret it as a signal that Chinese bonds are becoming increasingly acceptable not only for investment purposes but also as instruments of global financial infrastructure.

At the same time, Trump’s visit to China is becoming much more than a diplomatic event for financial markets. Investors increasingly view it as a turning point for:

- global economic growth;

- world trade flows;

- supply chain stability;

- the technology sector;

- the future of economic confrontation between the U.S. and China.

Markets are not reacting to the meeting itself, but to a much larger question: are Washington and Beijing moving toward managed competition, or is the world entering a new stage of accelerated economic fragmentation? The answer will likely determine the direction of U.S., European, and Asian equity markets for months ahead.

What this means for the S&P 500

The U.S. market remains less dependent on China than Europe or Asia. However, America still dominates the global technology sector, AI infrastructure, and the international reserve currency system.

For the S&P 500, a positive outcome of the summit — preservation of trade channels, delayed tariff escalation, and reduced geopolitical risks — could become a strong bullish catalyst. This is especially important for companies deeply integrated into global supply chains, including Apple, Nvidia, AMD, Qualcomm, Tesla, Microsoft, Amazon, Meta, Caterpillar, Boeing, Nike, and Starbucks.

Right now, institutional investors fear not so much a U.S. recession, but rather:

- new tariff escalation;

- pressure on Big Tech;

- disruptions in global supply chains;

- a geopolitical shock in commodity markets.

If negotiations fail, markets could quickly begin pricing in higher tariffs, weaker global trade, slower economic growth, and a new phase of technological confrontation between the U.S. and China.

The current rally in equities increasingly depends on political stabilization rather than purely economic fundamentals. Markets are effectively searching for protection from geopolitical fragmentation and trade aggression.

As long as uncertainty remains elevated, volatility may stay high even amid optimistic headlines.

So we act wisely and avoid unnecessary risks.

Profits to y’all!